Steps to Withdraw PF for Home Purchase or Construction in 2026 (Eligibility, Limits & EPFO Process)

8.3K

Learn how to use your PF withdrawal for buying a home, repaying a housing loan, or renovating your property in 2026. This guide covers eligibility criteria, withdrawal limits, document requirements, claim process using the UMANG App, and tax implications to make your PF withdrawal for property purchase easier and more efficient.

Contents

- PF Withdrawal for a Home Purchase in 2025: Conditions

- What is Partial PF Withdrawal?

- Different Types of PF Withdrawal for Property Purchase

- PF Withdrawal for Plot Purchase

- PF Withdrawal for Ready-to-Move-In House

- PF Withdrawal for House Renovation

- Documents Required: PF Withdrawal for Home Purchase

- Factors Leading to PF Withdrawal

- Umang App EPFO: PF Withdrawal Mobile App

- How to Withdraw PF Using Umang App by EPFO

- Tax Implications for PF Withdrawal for Property Purchase

- The Final Word

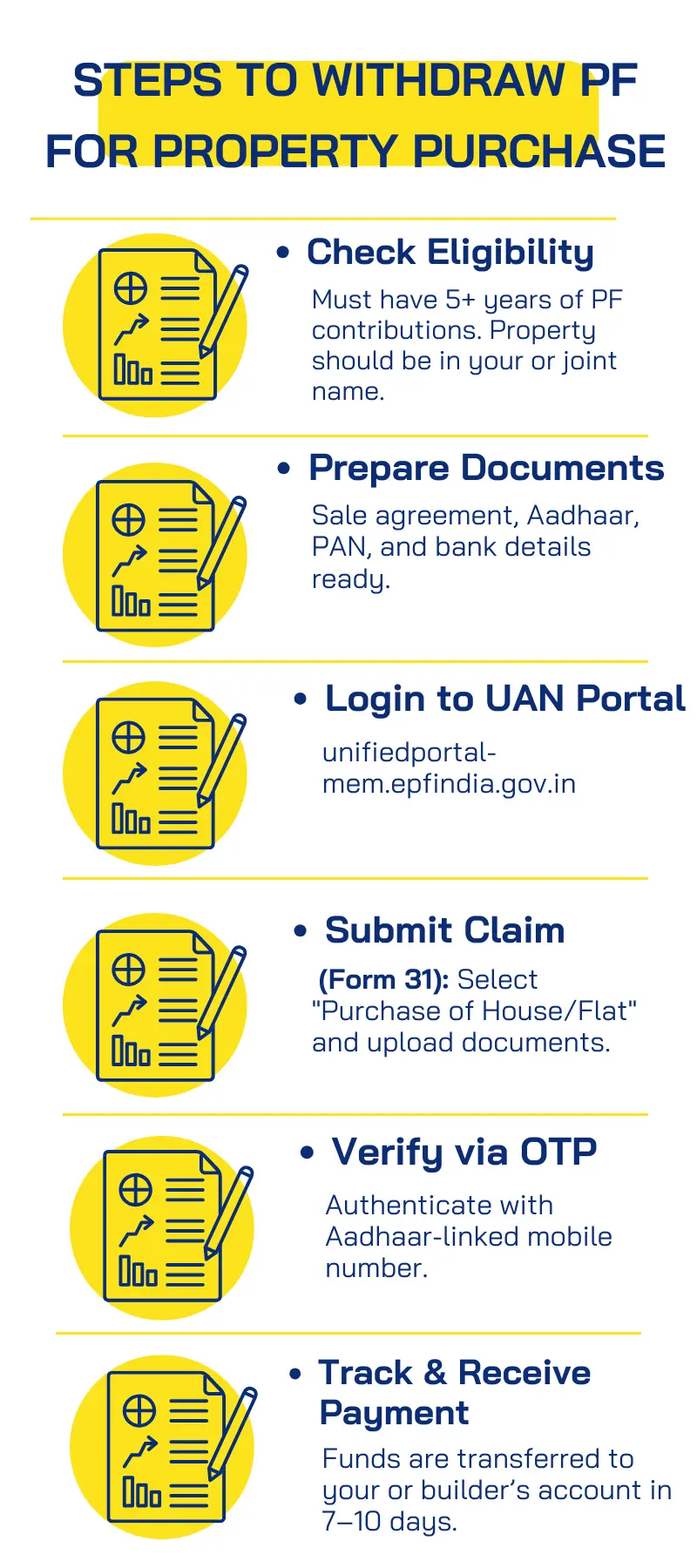

PF Withdrawal for a Home Purchase in 2025: Conditions

Before applying, it’s crucial to understand the eligibility conditions for PF withdrawal for house construction or property purchase in 2025:

- Minimum Service Requirement: You must have completed at least 5 years of continuous service with your employer.

- Usage of Withdrawn Funds: The funds can only be used for buying a plot, constructing a new house, purchasing a ready-to-move-in home, or even renovation/repairs of your existing property.

- Ownership Clause: The property should be in your name or jointly owned with your spouse. Properties owned by other family members do not qualify.

- Withdrawal Limit: The maximum withdrawal allowed is 90% of your total PF balance or the cost of the property, whichever is lower.

- Loan Repayment Option: PF funds can also be withdrawn to repay an existing home loan, provided the loan has been taken from a government-recognized lender.

- Timing of Application: Ensure the property purchase agreement is ready, as EPFO requires proof of intended use.

What is Partial PF Withdrawal?

Partial PF withdrawal allows you to access a portion of your PF savings before retirement. This feature is specifically designed to assist employees during major life events such as property purchase, medical emergencies, marriage, education, or house construction/renovation. Unlike complete withdrawal, you can still retain your PF account and continue contributing after making a partial withdrawal.

Different Types of PF Withdrawal for Property Purchase

PF Withdrawal for Plot Purchase

If you plan to buy a plot for residential use, you can withdraw up to 24 months’ basic salary + DA or the actual cost of the plot, whichever is lower. The plot must be purchased from a government-approved seller or housing authority.

PF Withdrawal for Ready-to-Move-In House

You can withdraw PF to buy a ready-to-move house from builders or housing boards. The withdrawal limit here is capped at 36 months’ basic salary + DA or 90% of the PF balance, whichever is lower.

PF Withdrawal for House Renovation

House repairs or renovations are also covered under PF withdrawal rules. To be eligible, the property should be at least 5 years old. The limit for withdrawal is 12 months’ basic salary + DA or the cost of renovation, whichever is lower.

Documents Required: PF Withdrawal for Home Purchase

To process your PF withdrawal for home purchase smoothly, ensure you have the following documents ready:

- Sale Agreement/Builder's Agreement: For property purchase or construction.

- Owner Declaration: Proof that the property is in your name or jointly owned with your spouse.

- Bank Account Details: Cancelled cheque of your linked bank account.

- Employer's Signature on Form 31: Approval for withdrawal.

- Other Supporting Documents: Invoices (for renovation) or loan details (for loan repayment).

Factors Leading to PF Withdrawal

- Property Purchase/Construction: To fund a plot or house.

- Home Loan Repayment: To reduce the financial burden of an existing loan.

- House Renovation/Repair: To upgrade or repair an existing property.

- Medical Emergencies: Covering healthcare costs.

- Marriage/Education Expenses: Supporting family needs.

Umang App EPFO: PF Withdrawal Mobile App

The Umang App (Unified Mobile Application for New-Age Governance) is a government initiative to simplify access to a range of services, including EPFO. With this app, employees can:

- Check their PF balance.

- File claims for PF withdrawal.

- Track withdrawal applications.

- Access EPFO passbook services.

This user-friendly app eliminates the need to visit EPFO offices, offering a convenient way to handle your PF needs.

How to Withdraw PF Using Umang App by EPFO

Follow these steps to withdraw PF using the Umang App EPFO:

- Download and Log In: Install the Umang app for PF and log in using your mobile number and OTP.

- Search for EPFO Services: Type “EPFO” in the search bar.

- Select ‘Raise Claim’: Navigate to the PF claim section.

- Enter Details: Fill in your UAN, property details, and reason for withdrawal.

- Upload Documents: Attach the required documents like sale agreement, cancelled cheque, etc.

- Submit the Claim: Review and submit your claim for processing.

Tax Implications for PF Withdrawal for Property Purchase

Withdrawals for property purchase are tax-exempt if you meet the required conditions (5 years of continuous service). However, if you withdraw your PF prematurely without meeting the conditions, the withdrawal will attract TDS (10%) unless your total income is below the taxable limit.

The Final Word

Using your PF savings for property purchase or construction is a prudent way to secure your future while avoiding excessive loans. However, it’s essential to adhere to the rules and ensure your decision aligns with your long-term financial goals. Whether you’re buying a plot, renovating your home, or repaying a loan, the EPFO and Umang App make the process efficient and hassle-free.